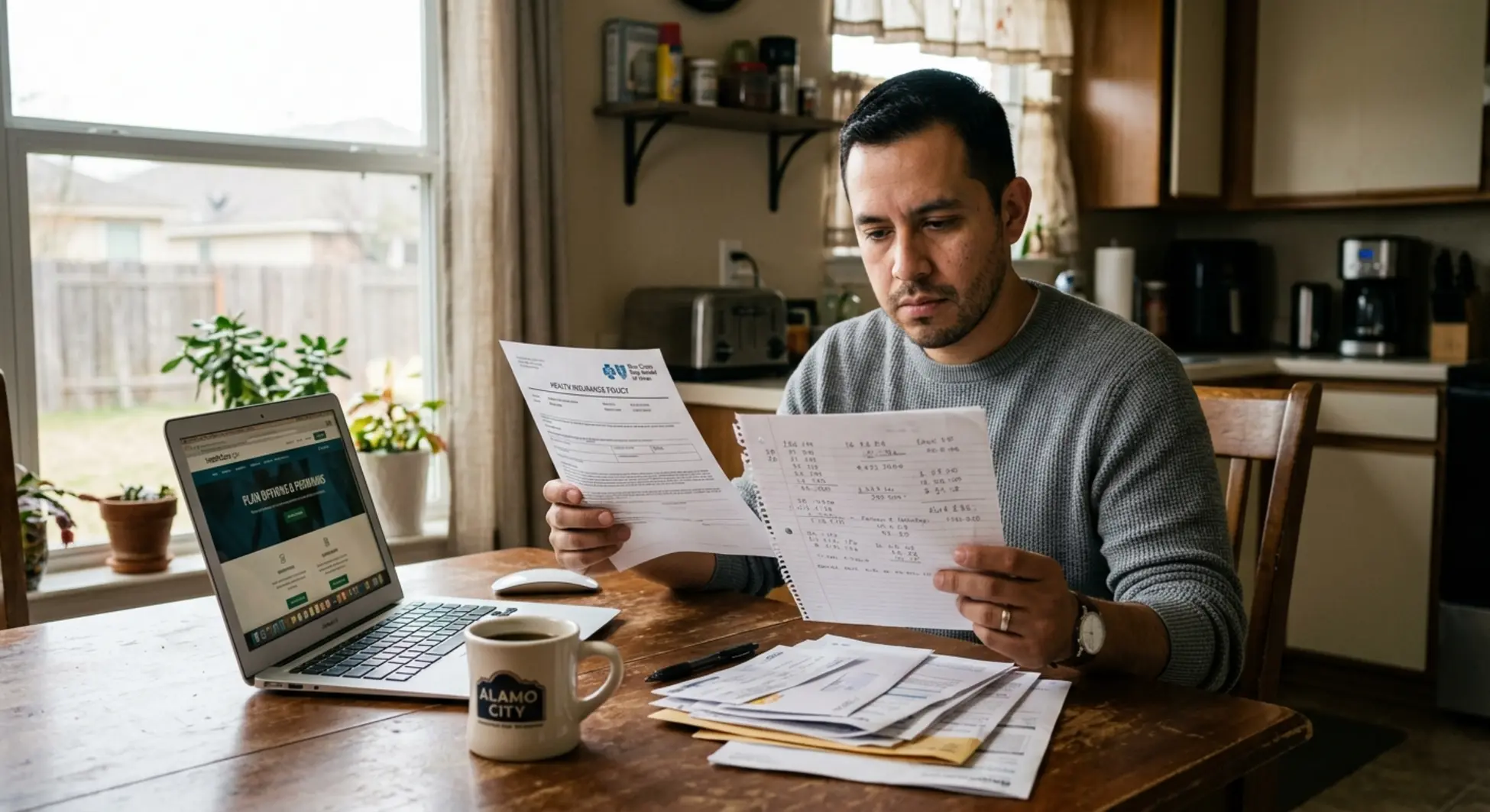

It’s 2am. Your son just called from treatment — his discharge date is in ten days — and you’re sitting at the kitchen table with your laptop open, typing “does insurance cover sober living” into a search bar, hoping someone out there has a straight answer. Or maybe you’re the one finishing up treatment, lying in your bunk, running the numbers in your head and wondering whether you can actually afford the next step. Either way, the anxiety is real, and the confusion is legitimate. The information out there is scattered, contradictory, and often written by people trying to sell you something.

Here’s what this guide is going to do: give you the honest, unvarnished answer to what insurance actually covers for sober living in Texas, what you’ll realistically pay out of pocket, and what your options are when the numbers feel impossible. No sales pitch. No false promises. Just the information you need to make a clear-headed decision about one of the most important transitions in a man’s recovery.

If you’re looking at sober living costs in Texas for the first time, the system can feel designed to confuse you. It isn’t — it’s just genuinely complicated. But once you understand how insurance thinks about housing versus treatment, and once you know where the real funding options are, you can stop spinning and start planning. Let’s get into it.

Key Takeaways

- Private insurance and Medicaid almost never cover sober living “rent” directly — less than 10% of sober living costs nationally are covered by insurance, and Texas follows that trend.

- Insurance CAN cover clinical treatment (IOP, therapy, MAT) that happens alongside sober living — that distinction is critical for budgeting.

- South Texas sober living costs range from $500–$1,800+ per month depending on structure, amenities, and certification level.

- Payment plans for move-in costs are often negotiable — always ask, especially about splitting the two-week upfront requirement into two payments.

- Funding alternatives exist: Oxford House interest-free loans, county SUD assistance, nonprofit grants, and HHSC-registered homes with sliding scale options.

- Families paying for sober living are not enabling — they’re investing in recovery. The key is structure: help with move-in, encourage the resident to contribute to ongoing costs.

- A 6-month stay ($4,500–$9,000) costs far less than a single relapse ($10,000–$50,000+). This is not an expense — it’s insurance against catastrophe.

The Hard Truth: What Insurance Actually Covers (and Doesn’t) for Sober Living

The number one misconception about paying for sober living — and it causes real harm to families and men in recovery — is the belief that health insurance will cover the cost of housing. It almost never does. Nationally, less than 10% of sober living costs are directly covered by insurance, and Texas has no state-specific insurance mandate that changes that equation. If you’ve been told otherwise, you’ve either been misled or the person talking to you doesn’t understand how the system works.

That said, insurance is not completely irrelevant to your situation. What it covers matters enormously for your overall budget — and understanding the line between what’s covered and what isn’t will help you plan without false hope or unnecessary panic. The short version: insurance covers clinical treatment. It does not cover housing. Those are two separate categories in the eyes of every major insurer, and the distinction is not a loophole — it’s how the system is designed.

Why Insurance Won’t Pay for Housing (Even Though It Feels Like It Should)

Sober living homes are classified as non-clinical supportive housing — not medical treatment facilities. Insurance is designed to cover medical necessity: therapy, detox, medication management, and clinical programs. Room and board, even in a structured recovery environment, doesn’t meet that definition. A treatment center is a licensed clinical facility; a sober living home is peer-support housing. These are fundamentally different categories under insurance law. Any home that tries to bill your insurance for housing costs as if they were clinical services is committing insurance fraud — and that’s a serious red flag, not a workaround.

What Your Insurance Might Cover While You’re in Sober Living

Here’s where insurance does show up, and it matters: if you’re attending an Intensive Outpatient Program (IOP) or outpatient therapy while living in a sober home, those clinical services are typically covered under your behavioral health benefits. The Mental Health Parity and Addiction Equity Act (MHPAEA) requires that insurance coverage for substance use disorder be no more restrictive than for medical or surgical conditions — so insurers are legally required to cover SUD treatment at the same level as other health conditions. That applies to therapy, IOP, medication-assisted treatment (MAT), and case management billed by a licensed provider.

What it does not apply to is the roof over your head. Parity covers treatment, not housing. So your practical strategy is this: use your insurance to cover every clinical service you can access — IOP, individual therapy, MAT if clinically indicated, psychiatric medication management — and budget separately for the housing cost. Those are two different line items, and treating them as such will give you a clearer picture of what you actually owe. To understand what the Drew’s program structure actually looks like day to day, that context helps you see exactly what you’re paying for and what your insurance might supplement on the clinical side.

Real Costs: What You’ll Actually Pay for Sober Living in South Texas

Transparency about money is rare in this industry, and it shouldn’t be. So here are the real numbers for men’s sober living in the San Antonio and New Braunfels area in 2026. The range is wide because the market includes everything from bare-bones shared rooms to structured, NARR-aligned homes with case management and programming. Knowing where different options fall helps you compare apples to apples.

| Tier | Monthly Cost Range | What You Typically Get |

|---|---|---|

| Basic / Low-Cost | $500 – $750/month | Shared rooms, minimal structured services, may not be NARR-certified |

| Mid-Range Structured | $750 – $1,200/month | Case management, group programming, accountability structure, NARR-aligned |

| Higher-End / NARR-Certified | $1,000 – $1,800+/month | Private or semi-private rooms, comprehensive programming, strong recovery support |

South Texas pricing is generally comparable to or slightly lower than the national average for similar quality homes, and meaningfully less expensive than Austin or coastal markets. That’s a real advantage for men in recovery in this region — the cost of living is lower, and there are legitimate options across the full price range.

Breaking Down the Move-In Cost

Move-in costs are where a lot of families get surprised, so let’s be specific. Most Texas sober living homes — including Drew’s — require two weeks of rent upfront at move-in, plus a one-time move-in fee. At Drew’s, that fee is $100. This is not a security deposit in the traditional sense, and most homes do not require “last month’s rent” the way a standard apartment lease would. Your total first-month cost is roughly 2.5 times your monthly rate, not double it.

So if you’re looking at a mid-range home at $900/month, your move-in day looks like: two weeks of rent ($450) plus a $100 move-in fee, totaling $550 upfront. The remaining two weeks of the first month are then due on the standard payment schedule. That’s a meaningful difference from what people often assume, and it makes the entry point more accessible than it initially appears. For specifics on Drew’s admissions process and move-in requirements, that page walks through exactly what to expect from application to arrival.

Hidden Costs Nobody Talks About

Beyond monthly rent and move-in, there are real ongoing costs that don’t show up in the headline number. Knowing these upfront prevents unpleasant surprises:

- Drug testing: $10–$40 per test, frequency varies by house rules. At Drew’s, daily breathalyzer testing and bi-weekly drug screening are built into the program. Ask any home how testing costs are handled — some include them in the monthly fee, others bill separately.

- Transportation: Getting to work, 12-step meetings, and outpatient appointments requires reliable transportation. Budget for public transit, ride-shares, or vehicle costs depending on your situation.

- Food: Residents at most sober living homes buy and prepare their own food. This is a real monthly expense — budget $200–$400/month depending on your eating habits.

- 12-step meeting contributions: Optional but customary, typically $1–$5 per meeting. At seven meetings a week, that’s $28–$140/month — manageable, but worth knowing.

- Savings minimums: Some structured programs require residents to save $50–$200/month as part of financial literacy training. This is money you keep — it’s building your exit fund — but it affects your monthly cash flow.

- Program fees: If a home offers specialized groups, case management, or add-on services beyond the base program, those may carry additional costs. Always ask what’s included in the monthly fee before you commit.

It’s Normal to Feel Overwhelmed by the Cost

Sober living isn’t cheap, and the fact that insurance won’t cover it feels unfair — because it kind of is. But here’s the reality: a 6-month stay ($4,500–$9,000) costs far less than a single relapse ($10,000–$50,000+). Research consistently shows men in structured sober living have sustained sobriety rates of 60–80%+ at 6–12 months, compared to 20–40% for men returning home directly after treatment. This isn’t an expense. It’s insurance against catastrophe.

The Real Cost of NOT Staying in Sober Living

This is the conversation that doesn’t get had enough. A single relapse — including re-treatment costs, emergency medical care, potential legal fees, and lost wages — typically runs $10,000–$50,000 or more. That’s not a scare tactic; that’s what the data from addiction policy research consistently shows. A 6-month stay in a mid-range sober living home costs $4,500–$9,000. The math is not subtle. The question isn’t whether you can afford sober living — it’s whether you can afford to skip it. Understanding the full picture of short-term versus long-term sober living and the outcomes research behind each can help you make that case to yourself or to your family.

Payment Plans & Sliding Scale Options: What’s Actually Available

Payment flexibility in sober living is real, but it varies significantly by operator type. Understanding who offers what — and how to have the conversation — can make the difference between a move-in that happens and one that doesn’t.

The most common form of flexibility is splitting the two-week upfront rent into two payments — one at move-in, one a week later. Most homes can accommodate this if you’re honest about your situation upfront. Move-in fees are sometimes waived or reduced for hardship cases, though this is less predictable. Ongoing payment plans for monthly rent are less common — most homes operate on a weekly or bi-weekly payment schedule rather than monthly, which itself provides some cash flow relief. Whatever arrangement you make, get it in writing. A verbal agreement that isn’t documented is worth nothing if there’s a dispute later.

Pro Tip: Ask About Move-In Flexibility

Most sober living homes can split the two-week upfront rent into two payments or work with you on timing. The move-in fee is sometimes negotiable. Always ask — the worst they can say is no, and many will work with you if you’re honest about your situation. The homes that won’t have that conversation at all are often the ones worth avoiding anyway.

Sliding Scale & Income-Based Pricing

Sliding scale pricing — where your monthly cost adjusts based on documented income — is more common in NARR-certified homes, nonprofit recovery residences, or homes that receive grant funding. Independent operators may have less structural flexibility, though many will work with residents on timing and payment arrangements when asked directly.

If you’re pursuing a sliding scale, expect to provide documentation: pay stubs, unemployment benefit statements, disability income records, or other proof of income. Most sliding scale programs have a minimum monthly floor — typically $400–$600 — below which they can’t go and still keep the lights on. And be aware that as your income increases, your rate typically adjusts upward. Transparency about that process matters: ask how and when rate adjustments happen before you sign anything. For families trying to understand how to navigate this conversation, the Drew’s resources for families page covers how to support your loved one through the financial planning process.

Trying to Figure Out What You Can Actually Afford?

That’s exactly what a conversation with Drew’s is designed to clarify. We work with real numbers and real situations — no pressure, no sales pitch. If you’re in your final weeks of treatment or just finished, reach out and we’ll talk through what’s realistic.

Financial Aid & Funding Sources: Beyond Insurance

Insurance isn’t the only funding mechanism available, and for many men in early recovery, it’s not the most important one. There are real alternatives worth knowing about — some require legwork, some require documentation, and some require timing. None of them are magic, but together they can make the difference between sober living being accessible and being out of reach.

Oxford House Loans & Self-Run Recovery Housing

Oxford Houses operate on a democratically run, peer-support model with no clinical staff. Monthly costs are typically $300–$600, making them among the most affordable structured recovery housing options available. The Oxford House organization provides interest-free loans to help residents cover move-in costs — a genuinely useful resource for men with limited immediate funds. Residents rotate leadership responsibilities, which builds accountability and ownership in a different way than staff-managed homes. Oxford Houses are a legitimate option for men who are self-motivated and need peer-driven structure without high costs. They’re not for everyone — the lack of clinical staff and structured programming means you need to bring your own discipline — but for the right person, they work.

State & County Funding for SUD Services

Texas HHSC operates a voluntary recovery residence registration program, and registered homes may have access to certain grant funding or state-level support. Bexar County and Comal County both maintain SUD treatment and support budgets, and county health departments can sometimes direct residents toward local assistance programs. DSHS — now part of HHSC — has historically funded some programs that offer subsidized housing or wraparound services. Eligibility varies significantly, and the application process can take time, so start early if you’re pursuing this route. Your best first call is to your county health department’s behavioral health division.

Nonprofit Grants & Scholarships

Local charities, faith-based organizations, and recovery-focused nonprofits sometimes offer grants or scholarships that can cover part of a sober living stay. These aren’t widely advertised, which is why most people don’t know they exist. Your treatment center’s discharge planner is often the best resource here — they know the local funding landscape and can make referrals. Searching “SUD recovery grants Bexar County” or “recovery housing assistance Comal County” can surface local options. Application timelines vary from days to weeks, so if you’re planning a move-in with a specific date, start the application process as early as possible. Some grants require proof of financial need; others prioritize specific populations such as veterans, men with young children, or men with criminal justice involvement. For a broader look at what to consider when choosing a sober living home in Texas, that guide covers the full evaluation framework.

Common Insurance Claim Denials & How to Appeal

Even when you’re pursuing coverage for legitimate clinical services — IOP, therapy, MAT — insurance denials happen. Understanding why they happen and what you can do about it is practical knowledge that can save you real money.

The most common denial scenario in the sober living context is this: someone attempts to bill housing costs as a covered treatment service, the insurer flags it as non-clinical, and the claim is denied. This is actually the correct outcome — housing isn’t a covered service, and billing it as one is fraud. But legitimate denials also happen for clinical services: lack of medical necessity documentation, provider credentialing issues, out-of-network status, or administrative errors.

What to Do If Your Claim Is Denied

First, request a written explanation of the denial from your insurance company. You need to know the specific reason before you can address it. Then gather documentation: clinical notes from your treatment provider, a description of the services provided, and any supporting evidence that the service was medically necessary. A letter from your treatment provider explicitly stating why the clinical service — and the supportive housing environment that enables you to access it — is medically necessary can significantly strengthen an appeal.

File your formal appeal within the timeframe specified in the denial letter — typically 30–60 days. Most insurance companies have a multi-level appeals process: internal appeal first, then external review if the internal appeal fails. Your treatment center’s billing team can often help navigate this process; they’ve done it before and know what documentation insurers respond to. If the denial amount is significant, consider engaging a patient advocate — they specialize in exactly this kind of negotiation and often work on contingency.

The Real Conversation to Have With Your Insurance Company

Don’t call general customer service. Call the behavioral health or SUD-specific line on the back of your insurance card. Ask specifically: “What SUD-related services are covered under my plan?” and “Does my plan cover any supportive housing or recovery support services?” Request a written summary of your SUD benefits. Clarify the difference between clinical treatment (covered) and housing (usually not). Ask about the appeals process and whether your plan has a patient advocacy resource. Get names and reference numbers for every call.

How to Spot Predatory Operators & Red Flags in Sober Living

This is the part of the guide that could save you from a genuinely bad experience. The sober living industry, like any industry serving vulnerable people, has operators who prioritize profit over resident welfare. Patient brokering — where homes pay kickbacks for referrals — is illegal in Texas and a major red flag. Fraudulent insurance billing, hidden fees, and pressure tactics are also warning signs that the home you’re considering isn’t operating with integrity.

Red Flag: Guaranteed Insurance Coverage Claims

If a sober living home promises that insurance will cover your housing costs, that is not true. Walk away immediately. Legitimate homes are transparent about what insurance covers (clinical treatment) and what it doesn’t (housing). Any home making this claim is either incompetent about how insurance works or is actively misleading you — neither is acceptable when you’re making a decision this important.

Beyond the insurance claim red flag, here’s what else to watch for: vague or evasive answers to direct questions, reluctance to provide written documentation of house rules and resident agreements, pressure to commit quickly or pay large upfront amounts, and difficulty understanding or canceling agreements. Legitimate operators answer direct questions directly. They provide documentation without being asked twice. They don’t need to pressure you because their program speaks for itself.

Questions to Ask Any Sober Living Home Before You Move In

Use this as your vetting checklist. A home that can’t or won’t answer these questions clearly is telling you something important:

Questions to Ask Before You Commit to Any Sober Living Home

- “Are you NARR certified or registered with Texas HHSC?” — legitimacy markers that indicate external accountability

- “What is your exact monthly cost, including all fees?” — the number should be specific and consistent

- “What is covered by the monthly fee — testing, groups, meals, transportation?” — clarity on what you’re actually paying for

- “Do you assist with insurance billing or offer sliding scale options?” — understanding their flexibility

- “What are your rules regarding employment, guests, curfews, and drug/alcohol testing?” — structure clarity

- “Can I see a sample copy of your house rules and resident agreement before I commit?” — documentation transparency

- “What happens if I need to leave early — what is your exit policy?” — exit clarity protects you

For a deeper look at what accountability-based recovery housing looks like from the inside — the daily structure, the testing protocols, the expectations — Drew’s program page lays it out without varnish. That’s the standard to compare other homes against.

Ready to Vet a Sober Living Home or Ask Hard Questions?

Drew’s Sober Living operates three houses in San Antonio and New Braunfels with transparent pricing, clear expectations, and no hidden fees. We answer every question on the list above — and we’ll give you honest answers, not a sales pitch. If you’re comparing options, we’re happy to be one of them.

NARR Certification & HHSC Registration: What They Mean for Your Coverage & Quality

You’ll hear these terms — NARR certification, HHSC registration — and it’s worth understanding what they actually mean, because they’re not just marketing language. They’re quality markers with real implications for accountability, funding access, and consumer protection.

What NARR Certification Actually Means

NARR stands for the National Association of Recovery Residences. It sets voluntary national standards for peer-support recovery housing — covering safety, resident rights, peer support quality, and recovery focus. Certified homes must meet specific criteria and undergo periodic compliance audits. In Texas, the state affiliate is TX-NARR, and certified homes are listed on the national NARR directory. Certification does not guarantee insurance coverage — nothing does, for housing — but it does signal that the home has committed to an external quality standard and is willing to be held accountable to it. That matters.

Texas HHSC Recovery Residence Registration

Texas HHSC operates a voluntary registration program for non-clinical recovery housing. Registered homes must meet baseline safety, operational, and resident rights standards. They’re listed on the HHSC recovery residence registry, which gives you a verifiable way to confirm a home’s legitimacy. Registration does not provide clinical licensure or insurance billing authority — those are separate systems — but it does mean the home has submitted to state-level oversight. Registered homes may also have access to certain state funding streams or grant opportunities that unregistered homes cannot access.

Why These Certifications Matter for Your Wallet

Certified and registered homes are more likely to have transparent pricing, documented policies, and access to grant or sliding scale funding. They’re easier to verify and hold accountable if something goes wrong. They’re also less likely to engage in the predatory practices — hidden fees, pressure tactics, fraudulent billing — that make some corners of the sober living market genuinely dangerous. Neither certification is a guarantee of a perfect experience, but both meaningfully reduce your risk. When you’re comparing homes, certification status is a legitimate filter to apply. For a comparison of what different types of recovery housing look like in practice, the sober living versus halfway house breakdown for Texas is worth reading before you make any decisions.

Payment Plans & Affordability at Drew’s Sober Living: How We Work With You

Drew’s operates three men’s recovery residences in South Texas: Chittim House in North San Antonio (10 beds), Evergreen House in Central San Antonio (8 beds), and Chapel Bend in New Braunfels (9 beds). Twenty-seven beds total, all running the same program. The pricing is transparent, the expectations are clear, and the conversation about money is one we’re willing to have directly.

We don’t promise insurance coverage for housing — because it doesn’t exist. What we do is help residents understand exactly what they’re paying for, coordinate directly with treatment centers to facilitate smooth transitions, and work with residents on move-in timing and payment flexibility when the situation calls for it. Our focus is on affordability and accountability, not luxury or hidden fees. If you want to know what a specific house looks like and what kind of resident does well there, the Drew’s house pages give you that detail.

What You’re Actually Paying For at Drew’s

This is the question worth asking of any sober living home, and we’ll answer it plainly. Your monthly cost at Drew’s covers:

What’s Included in Your Monthly Cost at Drew’s

- Daily breathalyzer testing — starts day one, no exceptions

- Bi-weekly drug screening — accountability built into the program, not added on

- Structured environment with clear house rules, assigned chores, and consistent expectations

- Brotherhood with other men in recovery — peer accountability and genuine community

- Coordination with your treatment team and ongoing case management support

- Financial literacy training — budgeting, savings habits, credit rebuilding

- Employment support and the 30-hour weekly work requirement framework

- Access to 12-step meeting culture and recovery community connections

That’s what the money buys. Not a room. A structure. A brotherhood. A set of daily habits that research shows correlate with sustained sobriety at rates of 60–80%+ at 6–12 months. The room is just where you sleep. The program is what changes things.

Here’s the honest version of the money conversation: we know you’re probably not flush with cash when you’re leaving treatment. Most guys aren’t. That’s not a character flaw — it’s just the reality of what addiction does to finances. What we ask is that you be straight with us about your situation so we can figure out what’s actually workable. We’re not running a charity, but we’re also not trying to squeeze you. We want men who are serious about recovery and willing to do the work. If that’s you, the money conversation is usually solvable.

The brotherhood you’ll find here — men who notice when you’re slipping, who show up for each other, who help the new guy find a meeting — that’s not something you can put a price on. But we’ll give you a fair one anyway.

How to Start the Conversation With Drew’s

Contact Drew’s during your final weeks of treatment or immediately after discharge. Be honest about your financial situation — that’s the only way to have a real conversation about what’s workable. Ask about move-in timing and payment options. Discuss your treatment team’s recommendations and whether a referral is in place. Expect a straightforward conversation about expectations, not a sales pitch. The application process at Drew’s is designed to be clear and fast — decisions typically happen within 24 hours of a completed application.

In Your Final Weeks of Treatment? Let’s Talk Now.

The best time to start the conversation about sober living is before you need it urgently. If you’re finishing up treatment in San Antonio or New Braunfels, reach out to Drew’s now to discuss move-in timing, payment options, and how we coordinate with your treatment team. The transition goes smoother when it’s planned, not scrambled.

For Families: How to Help Pay Without Enabling

If you’re a parent, spouse, or sibling reading this at 2am wondering whether paying for sober living is just another way of enabling your loved one — it isn’t. Paying for structured, accountable recovery housing is fundamentally different from paying for an apartment with no expectations, covering bills while someone avoids treatment, or handing over cash with no accountability attached. Sober living comes with structure, testing, rules, and consequences. You’re not removing accountability — you’re funding the environment where accountability happens.

For Families: Paying for Sober Living Is Not Enabling

If you’re a parent or spouse considering helping with sober living costs, that’s not enabling — it’s investing in recovery. Set clear boundaries: you help with move-in, the resident contributes to ongoing costs as employment develops. Encourage financial responsibility as part of the recovery process, and let the resident manage the relationship with the home directly. That’s how you support without undermining the accountability that makes sober living work.

The practical framework that works best: families help with move-in costs (the upfront two weeks plus the move-in fee), and the resident takes responsibility for ongoing monthly costs as employment develops. This creates a clear handoff — you’re providing the bridge, they’re building the foundation. Avoid paying the home directly on an ongoing basis if possible; let the resident manage that relationship. It builds financial responsibility and keeps the accountability structure intact. For more on how to support a loved one through early recovery without overstepping, the Drew’s family resources page addresses the most common questions families bring to us.

Frequently Asked Questions

Does insurance cover the cost of sober living homes in Texas?

Generally, no. Private insurance and Medicaid do not directly cover sober living “rent” or housing costs. Nationally, less than 10% of sober living costs are covered by insurance, and Texas has no state mandate that changes this. Insurance may cover clinical treatment — like IOP or therapy — that a resident attends while living in a sober home, but the housing itself is classified as non-clinical supportive housing and falls outside covered benefits. Some NARR-certified or HHSC-registered homes may help residents navigate limited funding sources or sliding scale options, but direct insurance coverage for housing remains rare in 2026.

Can I use my health insurance for sober living if it’s considered a mental health or SUD benefit?

Sober living homes are classified as non-clinical housing, not direct mental health or SUD treatment — so even robust behavioral health benefits typically don’t cover the housing cost. The Mental Health Parity and Addiction Equity Act requires equal coverage for mental health and SUD services, but insurers distinguish between medical treatment (covered) and housing support (not covered). What parity does help with is ensuring your IOP, therapy, and MAT are covered at the same level as other medical services while you’re living in sober housing. Always verify your specific SUD benefits by calling your insurer’s behavioral health line directly — and get the summary in writing.

What if my insurance denies coverage for sober living or related services? Can I appeal?

Yes — you have the right to appeal any insurance denial, and you should. Start by requesting a written explanation of the denial from your insurer, which will specify the exact reason. Gather documentation from your treatment provider, including clinical notes and a letter explaining why the service is medically necessary. File your formal appeal within the timeframe specified in the denial letter — typically 30–60 days. Your treatment center’s billing team can often help navigate this process, and a patient advocate is worth considering if the denial amount is significant. External review is available if your internal appeal is unsuccessful.

Are payment plans or sliding scales common for sober living homes in Texas?

Payment plans for move-in costs are sometimes negotiable — most homes can split the two-week upfront rent into two payments if you ask directly and are honest about your situation. Sliding scale pricing is more common in NARR-certified homes, nonprofit residences, or homes receiving grant funding; independent operators may have less structural flexibility but often work with residents on timing. Sliding scales typically require proof of income — pay stubs, unemployment benefits, disability documentation — and have a minimum monthly floor, usually $400–$600. Whatever flexibility you negotiate, get it in writing before you move in.

How can I pay for sober living if I am unemployed or have limited income?

Several options exist beyond self-pay: Oxford House provides interest-free loans to help cover move-in costs for their peer-run homes; Bexar County and Comal County both have SUD treatment and support budgets that may include housing assistance; local nonprofits and faith-based organizations sometimes offer grants or scholarships for sober living; and HHSC-registered homes may have access to state funding streams. Most structured programs, including Drew’s, require active job seeking as part of the recovery process — employment is part of the program, not just a nice-to-have. Starting the funding conversation early, ideally while still in treatment, gives you the most options.

What are the biggest red flags when choosing a sober living home?

The clearest red flag is any claim of “guaranteed insurance coverage” for housing — that’s false, and any home making that claim is either misinformed or actively deceptive. Beyond that, watch for vague or evasive answers to direct pricing questions, reluctance to provide written documentation of house rules and resident agreements, pressure to commit quickly or pay large upfront amounts, and lack of verifiable credentials like NARR certification or HHSC registration. Legitimate homes answer direct questions directly, provide documentation without being pushed, and don’t need high-pressure tactics because their program stands on its own merits. Patient brokering — where homes pay kickbacks for referrals — is illegal in Texas and a serious warning sign.

A man finishes his last week of treatment, and the question that’s been sitting in the back of his mind finally comes to the front: now what? He’s done the work. He’s been honest in group. He’s made the calls he needed to make. But the gap between where he is and where he needs to be — a job, a routine, a place where sobriety is the expectation, not the exception — feels enormous. He types “does insurance cover sober living” into his phone at 11pm and gets a wall of confusing, contradictory information.

What he actually needs is someone to tell him the truth: insurance probably won’t cover the housing, but here’s what it will cover. Here’s what you’ll actually pay. Here’s how to have the conversation about move-in flexibility. Here’s where to look if the numbers feel impossible. And here’s what you’re actually buying when you invest in a structured recovery home — not a room, not a program to complete, but a brotherhood of men who will notice when you’re slipping and say something about it. Men who show up. Men who are building the same thing you are.

That’s what sober living is. And that’s what’s worth paying for.

Still Have Questions About Insurance, Costs, or Whether Sober Living Is Right for You?

We know the money conversation is hard, and we know the system isn’t designed to make it easy. If you’re a man finishing treatment, a family member trying to help, or a treatment center looking for a trusted referral partner in South Texas — we’re here to listen and help you figure out the next step. No pressure. Just honest conversation about what’s real and what’s workable.

Drew’s Sober Living · Men’s Recovery Residences in San Antonio & New Braunfels, TX